Despite living in times where many families are struggling with the rising costs of energy, food and fuel, the start of the 2022/23 tax year brings more unwelcome costs due to tax increases as the Government looks to make up the shortfall from the pandemic. The Prime Minister has faced calls to re-think the proposed increases and freezes outlined by The Chancellor in his October 2021 budget, however in a joint article for the Sunday Times in January, they confirmed their commitment to the original proposal. So, what does this mean for individuals and businesses across the UK as we near the start of a new tax year?

Changes to National Insurance

National Insurance rates will increase by 1.25% from 6th April 2022. According to the government, the tax increase is intended to generate revenue for the NHS and social care.

From 2023, the rate of National Insurance will return to 2021/22 levels. However, it will be replaced with a 1.25% Heath and Social Care Levy.

Starting from 6th April 2022, the lower earnings limit will rise by 3.1%. The rate increase will apply to both the middle and upper earnings thresholds. However, the upper earnings threshold will stay frozen at £50,270. See below the breakdown of the National Insurance changes for both employed and self-employed individuals.

Class 1 NICs

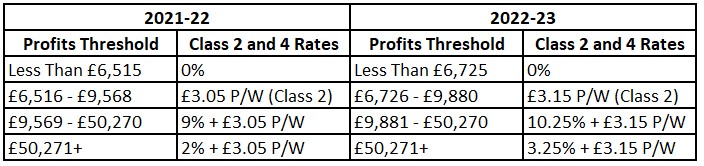

Class 2 and 4 NICs

Class 2 and 4 NICs

You will likely pay Class 2 and 4 NICs if you are self-employed, depending on your earnings.

Class 3 NICs

Class 3 NICs

This class applies to voluntary contributions. For example, if you have gaps in your record to positive affect your eligibility for State Pension and other benefits. In 2021-22 this was £15.40 per week, rising to £15.85 per week in 2022/23.

Dividend tax rates increase

Similarly, to the National Insurance rate rises, those who earn money from dividends will also see a 1.25 percentage point rise from April. You may have to pay dividend tax if you hold shares in a company, and your earnings via this source exceeds the dividend allowance, which remains at £2,000 in 2022/23.

Rates of income tax in 2022

Despite the changes across the board to tax in 2022, income tax rates have remained frozen at those of the previous tax year. The personal allowance, how much you can earn before income tax applies, also remains the same.

Capital gains tax in relation to property sales

The changes here actually went live at the point the budget was announced, however it can be something that is easily missed, so it’s always good to cover whenever it comes up.

You previously had 30 days to report any gains made from the sale of your property and pay the tax you owed to HMRC on any gain made. This window has now increased to 60 days, but no amendments to rates or thresholds come into effect.

The changes were brought in to allow for delays suffered obtaining the correct reference numbers and online accounts to make the report to HMRC.

Frozen thresholds

The inheritance tax thresholds – the nil-rate band (£325,000) and residence nil-rate band (£175,000) – and the pensions lifetime allowance (£1,073,100) will be maintained at their existing levels until April 2026.

The UK VAT-registration and deregistration threshold follow suit and remain at their existing £85,000 and £83,000 respectively.

Accountant for New Business Start Up, Accountants in Wigan, Bookkeeping Services, Finance Performance, Outsourced Bookkeeping, Outsourcing Payroll & Pensions, Payroll In Wigan, Personal TAX Wigan, Setting Up a Business Wigan, Supporting Loan Applications Wigan, VAT Return,