As a small, growing business you will quickly become aware of the UK’s VAT system. In simple terms, you must register for VAT if:

- You expect your VAT taxable turnover to be more than £85,000 in the next 30-day period, or;

- Your business had a VAT taxable turnover of more than £85,000 over the last 12 months.

You can also register voluntarily if you do not meet either of the conditions above.

So, if you’re registered for VAT, you’ll need to decide which accounting scheme you will use to account for your VAT. The most common schemes that businesses utilise are invoice accounting for VAT, commonly referred to as the ‘accrual method’, or cash accounting for VAT. In our previous article, we covered another VAT scheme that is used by some businesses, the Flat Rate VAT Scheme, so feel free to check it out here! Which scheme you choose will depend upon a number of factors: the size of the business, individual needs and the cash flow position of the business.

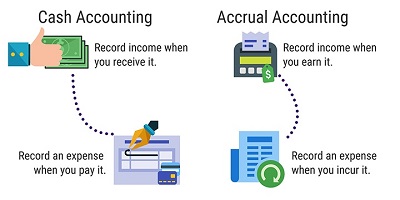

What is Cash Accounting for VAT?

Businesses that use cash basis accounting recognise income and expenses only when money changes hands. They don’t count sent invoices as income, or bills as expenses – until they’ve been settled.

Let’s look at an example:

A business prepares its VAT Returns to the 31st March, 30th June, 30th September and 31st December.

On 1st February a business issues an invoice to a customer for £2,000 + VAT (a total of £2,400). The VAT is charged at the standard rate of 20%, so the business will have to pay £400 to HMRC.

The customer pays the invoice on 1st April. The £400 in VAT that must be paid to HMRC must be included on the return for the quarter ending 30th June, rather than the return for the quarter ending 31st March, as the invoice was not paid in the same VAT period that it was raised in.

You can use cash accounting if:

- Your business is registered for VAT.

- Your estimated VAT taxable turnover is £1.35 million or less in the next 12 months.

You cannot use cash accounting if:

- You use the Flat Rate VAT Scheme – this scheme uses its own cash-based method.

- You aren’t up to date with your VAT Returns or payments.

- You have committed a VAT offence in the last 12 months.

You cannot use cash accounting for the following transactions (you must use accrual VAT accounting instead):

- Where the payment terms of a VAT invoice are 6 months or more

- Where a VAT invoice is raised in advance

- Buying or selling goods using lease purchase, hire purchase, conditional sale or credit sale

- Importing goods into Northern Ireland from the EU

- Moving goods outside a customs warehouse

You must leave the cash accounting scheme if your VAT taxable turnover is more than £1.6 million.

Leaving the cash accounting scheme

You can only leave the cash accounting scheme at the end of a tax period. After you have left the scheme, you must then use the invoice accounting method from the beginning of the next tax period. HMRC provides detailed information on leaving the scheme in this VAT notice, but remember to get in touch if you’re in any doubt.

What is Accrual Accounting for VAT?

Businesses that use accrual accounting recognise income as soon as they raise an invoice for a customer. When a bill comes in, it’s recognised as an expense even if payment won’t be made immediately.

Using the same example as we looked at for the cash accounting scheme, it must include the £400 from the invoice on its 31st March VAT Return, as it must be included the return that covers the date of the invoice, not the date of the payment.

If you use the accrual accounting scheme, you can reclaim the VAT you pay to your suppliers in the period which your supplier invoices you, whereas using the cash accounting scheme only allows you to reclaim VAT once you have paid your supplier.

If you tend to pay your bills promptly, it won’t make a big difference if you use the accrual or the cash accounting scheme. However, if your customers always pay you immediately, then you may be better off sticking to invoice accounting so that you can reclaim the VAT promptly on your bills from your suppliers.

What if a payment is received before you send an invoice?

If a customer pays you before you have invoiced them, you are liable to pay the VAT at the point the customer paid you even if you’re using the invoice accounting scheme for VAT. This is because a payment from a customer creates a tax point (i.e. a point at which VAT becomes payable).

If you would like to know more about the Accountancy Services we offer, then the easiest way to do it is to go to our website and take it from there!

If you’re still unsure about us, you can see our full testimonial page at testimonials

Interested in contacting us in regard to this post or have another question you would like us to answer? You can phone or email our office. More information on contacting us at contacts

Accountant for New Business Start Up, Accountants in Wigan, Bookkeeping Services, Finance Performance, Outsourced Bookkeeping, Outsourcing Payroll & Pensions, Payroll In Wigan, Personal TAX Wigan, Setting Up a Business Wigan, Supporting Loan Applications Wigan, VAT Return,