Under the current rules for determining which profits of an unincorporated business are taxed in a particular tax year, some profits may fall to be taxed twice in the opening years of a business. These profits are known as overlap profits.

Once the business is up and running, the profits that are currently taxed for a particular tax year are those for the accounting period that ends in the tax year. This is known as the current year basis. Most commonly, owners of unincorporated businesses are taxed on their earnings between 6th April and 5th April of the following year, in line with the tax year. However, it is possible to set your own accounting date as an unincorporated business – perhaps if you set up part way through a tax year.

For example, if an established sole trader prepares accounts to 30 June each year, they will be taxed on the profits for the year to 30th June 2021 in the 2021/22 tax year, as this is the period that ends in that tax year. If the business then chooses to change their accounting date once the business is up and running, there may be overlap profits and relief may be available for those profits that are taxed twice.

How are profits taxed in the early years as an unincorporated business?

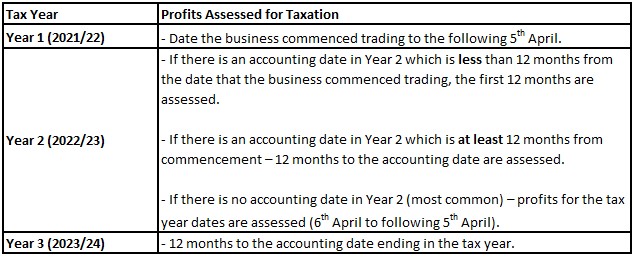

This is easier to look at using an example:

Jane is a sole trader who commenced trading on the 1st June 2017. She prepares her accounts to 30th April each year. In her opening tax years as an unincorporated business, the following profits were assessed for taxation:

As you can see from the dates above, the profits for the period 1st June 2017 to 5th April 2018 are assessed and taxed in both Year 1 and Year 2. These are Jane’s overlap profits.

Overlap relief on a change of accounting date

If on a change of accounting date, the new accounting date is more than 12 months from the old accounting date, and the trader has overlap profits which have yet to be relieved, overlap relief may be given on the change of accounting date. Overlap relief is given by deducting the overlap profits from the profits for the tax year in which the change of accounting date occurs. The relief is restricted to the number of days in the overlap period and the number of days the change of accounting date exceeds 12 months.

Overlap relief in final year of trading

Under the current rules, if overlap profits have not been relieved when the business ceases, relief is given by deducting the overlap profits from the profits assessed in the final tax year.

Basis period changes

The basis period rules are being reformed, moving to a tax-year only basis from 2024/25. The 2023/24 tax year will be a transitional year in which relief for any unrelieved overlap profits will be given to unincorporated businesses who are eligible. We have covered the reform in more depth previously on the blog.

Our team of experienced professionals are on hand to help with any of your needs regarding overlap relief claims, and advice on changes to accounting periods, so get in touch today!

Accountant for New Business Start Up, Accountants in Wigan, Bookkeeping Services, Finance Performance, Outsourced Bookkeeping, Outsourcing Payroll & Pensions, Payroll In Wigan, Personal TAX Wigan, Setting Up a Business Wigan, Supporting Loan Applications Wigan, VAT Return,